Open finance is a secure data-sharing standard that connects someone’s financial life to the apps and services they use. It allows the bank, the insurance provider, and the pension fund to share information through secure "digital pipes" called APIs. In the past, financial data lived in "silos"—the bank didn't know about a customer’s investments, and their budgeting app couldn't see their mortgage. Open finance connects all financial accounts together.

Key takeaways

Open finance is a technical standard that allows different financial accounts (insurance, retirement, bank, investments) to securely “talk” to each other.

Application programming interfaces (APIs) are the secure digital pipes that get data from one financial account to the next.

Consumers gain greater control over their own financial data through explicit consent mechanisms in the open finance framework.

Financial institutions and fintechs can build innovative financial products and services on shared data.

Strong governance, privacy controls, and secure data sharing standards are essential for trust and compliance.

Table of contents

- Open finance allows separate accounts to connect

- Open finance vs. open banking vs. open data

- How open finance started

- How open finance works

- Principles of open finance

- Benefits of open finance

- Risks and security concerns

- Common use cases

- Open finance technologies: APIs and data infrastructure

- The future of open finance

- Related resources

- FAQs

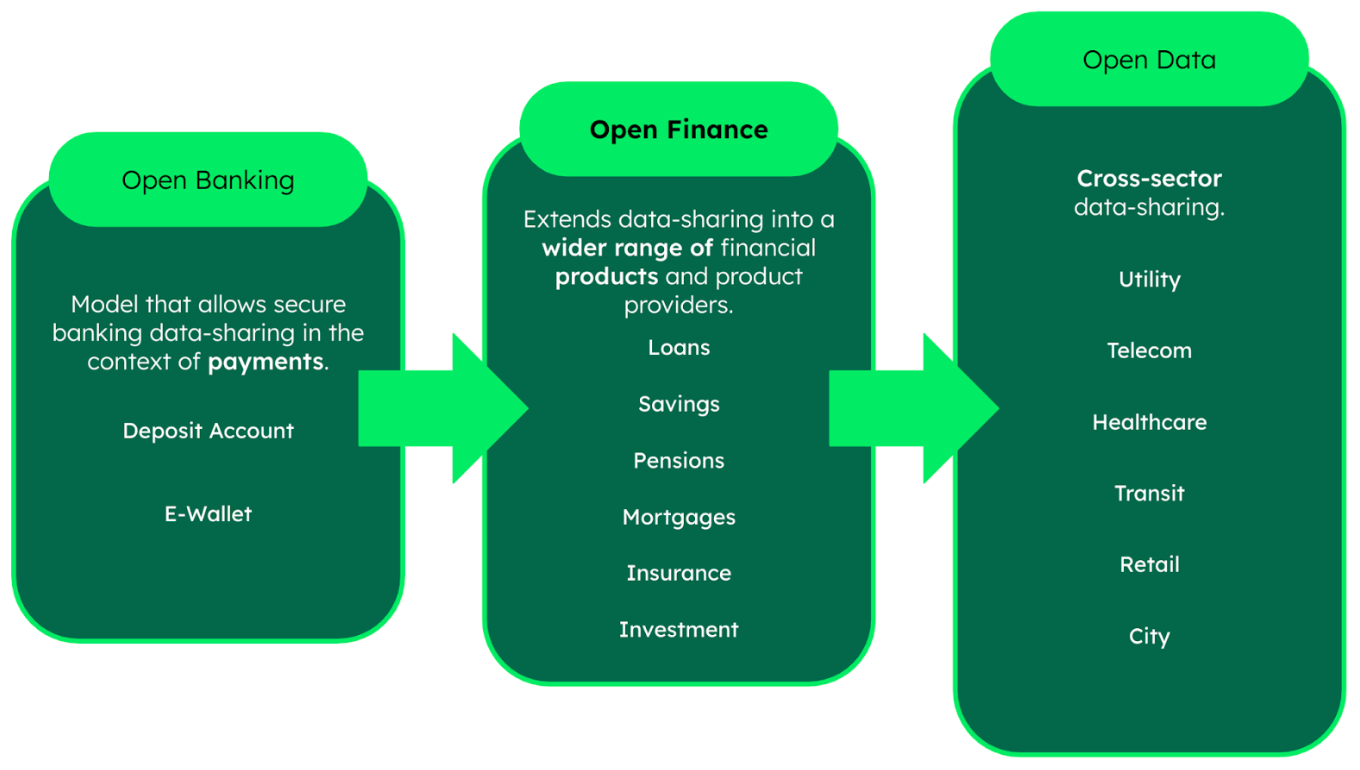

Open finance allows separate accounts to connect

In the financial services industry, open finance is a framework that enables consumers and businesses to securely share their financial data with authorized third parties, typically through application programming interfaces. It expands on open banking by extending data access beyond bank accounts to a broader range of financial products and services, including savings accounts, investment platforms, pensions, insurance, and lending.

At its core, open finance shifts control of financial data from institutions to individuals. Consumers can grant explicit and informed consent for financial data access, enabling connected financial apps and services to analyze their financial situation, deliver tailored products and services, and help make more informed decisions.

Open finance vs. open banking vs. open data

Open finance is often confused with adjacent, related terms. But clear distinctions exist.

Open banking focuses primarily on banking data, such as checking and savings accounts, and payment initiation. It was formalized in many regions through regulatory initiatives like Payment Services Directive 2, requiring banks to provide secure API access to licensed third-party providers for payment account data and payment initiation.

Open finance, however, encompasses financial data exchange across a wide range of financial products, including investments, insurance policies, mortgages, pensions, and other financial accounts. It creates a broader, open finance ecosystem that includes traditional financial institutions, fintech startups, and other financial service providers.

Open data is even broader. It refers to publicly available datasets that can be accessed and reused by anyone, often without restriction. It is not limited to financial services and doesn't necessarily involve consumer consent.

How open finance started

Open finance evolved from regulatory efforts in the financial industry to increase competition and improve consumer rights.

In the European Union, the Payment Services Directive 2 mandated that banks provide secure APIs to enable data access for licensed third parties. The United Kingdom expanded this through Open Banking Limited, which standardized API specifications and security protocols.

These open banking frameworks demonstrated that secure financial data sharing could unlock innovation. Regulators and industry bodies began exploring how similar principles could apply beyond bank accounts, leading to broader open finance systems.

Today, open finance frameworks are emerging globally, supported by financial data access regulation and consumer data rights initiatives.

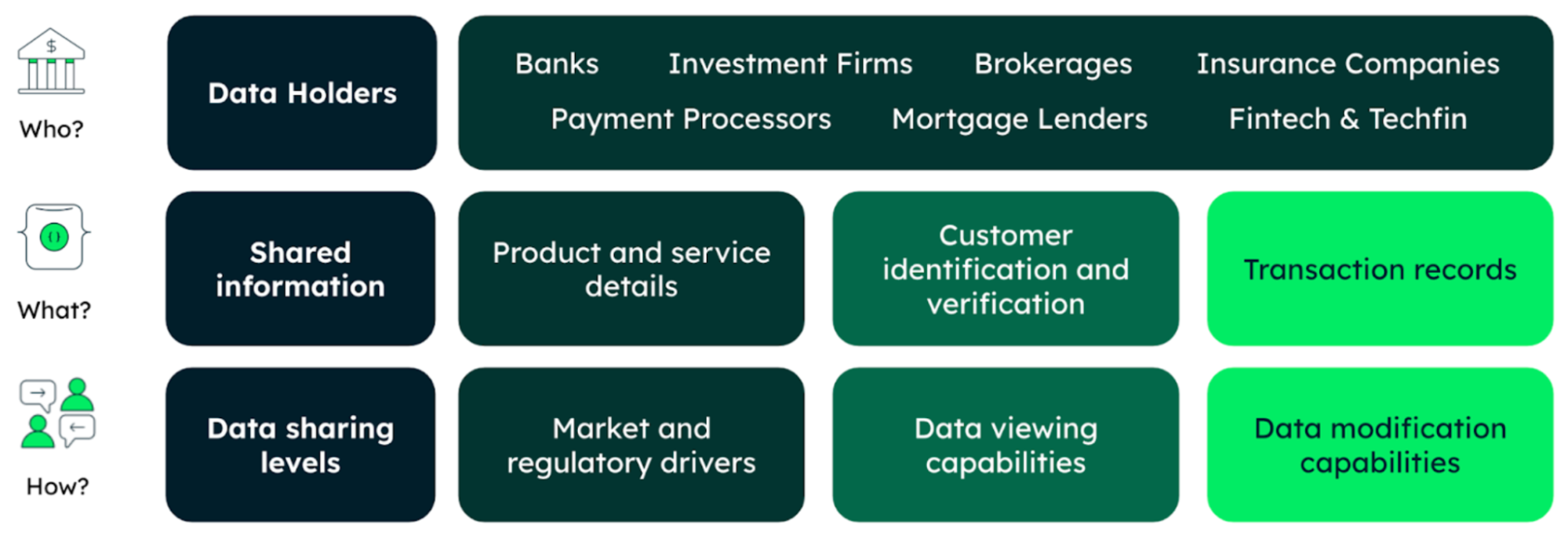

How open finance works

Open finance relies on structured, secure data exchange between multiple actors in the financial ecosystem.

A simplified flow looks like this:

A customer provides explicit and informed consent to share financial data.

Data holders, such as banks, insurers, or investment platforms, expose data via secure APIs.

Data users, such as fintechs or financial apps, request access.

Connectivity providers, or API gateways, facilitate secure data exchange.

Regulators define industry standards and monitor compliance.

Application programming interfaces are the backbone of open finance technology. They allow systems to share financial data access in near real time, while maintaining authentication, authorization, and audit trails.

This structured approach enables secure data sharing without forcing consumers to disclose login credentials. It aims to replace screen scraping (giving an app your password) with standardized, permission-based financial data exchange.

Principles of open finance

Open finance is guided by several foundational principles:

Consumer consent: Data sharing must be permission-based and revocable.

Transparency: Consumers receive clear and accessible information about how their customer data is used.

Security and privacy: Systems must protect consumer data against breaches and misuse.

Interoperability: Industry standards ensure different financial platforms can communicate.

Accountability: Financial institutions and fintechs are responsible for protecting customers’ financial data.

These principles build trust and support sustainable open finance adoption.

Benefits of open finance

For consumers

Open finance benefits consumers by giving them greater visibility into their financial lives. Improved financial inclusion is another benefit. Individuals with limited traditional credit histories can demonstrate creditworthiness using broader financial data.

Financial apps can aggregate transaction data across multiple bank accounts and investment platforms, enabling budgeting apps, credit decisioning tools, and financial health dashboards. Consumers gain access to more competitive financial products and services tailored to their needs.

For financial institutions

Traditional financial institutions can innovate more quickly by participating in the open finance ecosystem. Secure data sharing allows them to collaborate with fintechs, launch embedded finance offerings, and reduce friction in onboarding and lending processes. Structured data access can also reduce operational costs and enhance customer experience.

For fintechs

Fintechs can build new open finance solutions without owning the entire infrastructure stack. With authorized access to financial accounts, they can design specialized financial services, from payment initiation to real-time investment analysis, accelerating innovation in the financial services industry.

Risks and security concerns

Open finance introduces new security concerns alongside its benefits. More financial data exchange increases the attack surface. Protecting consumer data requires robust encryption, strong authentication and strict access controls. Poorly designed APIs or weak governance can expose sensitive information.

There are also compliance implications. Regulations such as the General Data Protection Regulation (GDPR) impose strict requirements on data access, storage, and consent management. Organizations must ensure that open finance systems align with privacy laws and industry standards.

Operational risks include data quality issues and inconsistent schemas across data providers. Without strong governance, financial data sharing can become fragmented and unreliable.

Common use cases

Open finance is used across a range of financial apps and services:

Personal financial management: Aggregating bank accounts, savings accounts, and investment platforms in one dashboard.

Credit decisioning: Using transaction data to assess affordability and risk.

Embedded finance: Integrating financial services into non-financial platforms.

Wealth management: Consolidating views of financial accounts and portfolios.

Insurance underwriting: Accessing broader financial data improves risk modeling.

These use cases depend on secure, real-time data access across the financial ecosystem.

Open finance technologies: APIs and data infrastructure

Application programming interfaces are central to open finance technology, but APIs alone are insufficient.

Organizations must manage structured, semi-structured, and unstructured open finance data across multiple data providers. They need scalable systems that support evolving schemas, high-volume transaction data, and strict compliance requirements.

A flexible data platform enables financial institutions and fintechs to ingest diverse financial data exchange formats, enforce governance policies, and power analytics and AI use cases.

Modern data architectures also prepare organizations for the AI age, where machine learning models rely on high-quality, well-governed financial data access.

The future of open finance

Open finance adoption is expected to accelerate as regulators clarify standards and consumers demand more control over their own financial data.

Future developments may include:

Expansion into pensions, healthcare finance and tax data.

Greater interoperability across borders.

Stronger consumer data rights frameworks.

Deeper integration with AI-driven financial platforms.

As the financial landscape evolves, open finance systems will become foundational infrastructure for digital financial services.

Related resources

- MongoDB powers open finance with flexible data integration, built-in security, and scalable financial services.

- Demo: Embracing Open Finance Innovation with MongoDB walks you through the basics.

- MongoDB encryption capabilities that help protect financial data at rest and in transit.

- MongoDB Queryable Encryption overview, explaining how encrypted fields can still be queried, which is critical when managing sensitive customer data in open finance systems.

- Encryption at rest helps protect consumer data and customer's financial data.

- See how MongoDB Atlas supports encryption at rest using customer key management.

- MongoDB case studies in financial services.