Traditional lending systems rely on disconnected legacy applications that were never designed for real-time data, automation, or digital-first customer experiences. Today, customers expect instant decisions, seamless digital experiences, and immediate transparency, while lenders must manage rising risk, regulatory pressure, and data complexity. Modern digital lending platforms are transforming this reality by unifying origination, decisioning, funding, and servicing into a single, intelligent workflow. In this article, we break down the end-to-end digital lending lifecycle and show how data-driven architectures are redefining how loans are created, approved, funded, and managed instantaneously.

Available Languages

Digital lending is no longer optional; it is now a strategic imperative for lenders.

According to McKinsey1, AI agents are taking over manual, rule-based execution like collecting borrower information and drafting credit reports, shifting employees from spending 80% of their time on manual tasks to spending 80% of their time engaging with customers and making key decisions.

The next evolution of digital lending is being driven by intelligent agentic AI systems that do not just process data, but also actively reason, act, and adapt across the lending lifecycle. Unlike traditional automation or static models, agentic AI proactively works for you behind the scenes while:

Orchestrating tasks across loan origination, underwriting, servicing, and renewal.

Continuously learning from new data and changing borrowers and lenders conditions.

Detecting credit risks, personalizing borrower journeys, and even triggering underwriting workflow decisions in real time.

For lenders, this marks a shift from reactive operations to self-optimizing lending platforms that scale with confidence, resilience, and speed.

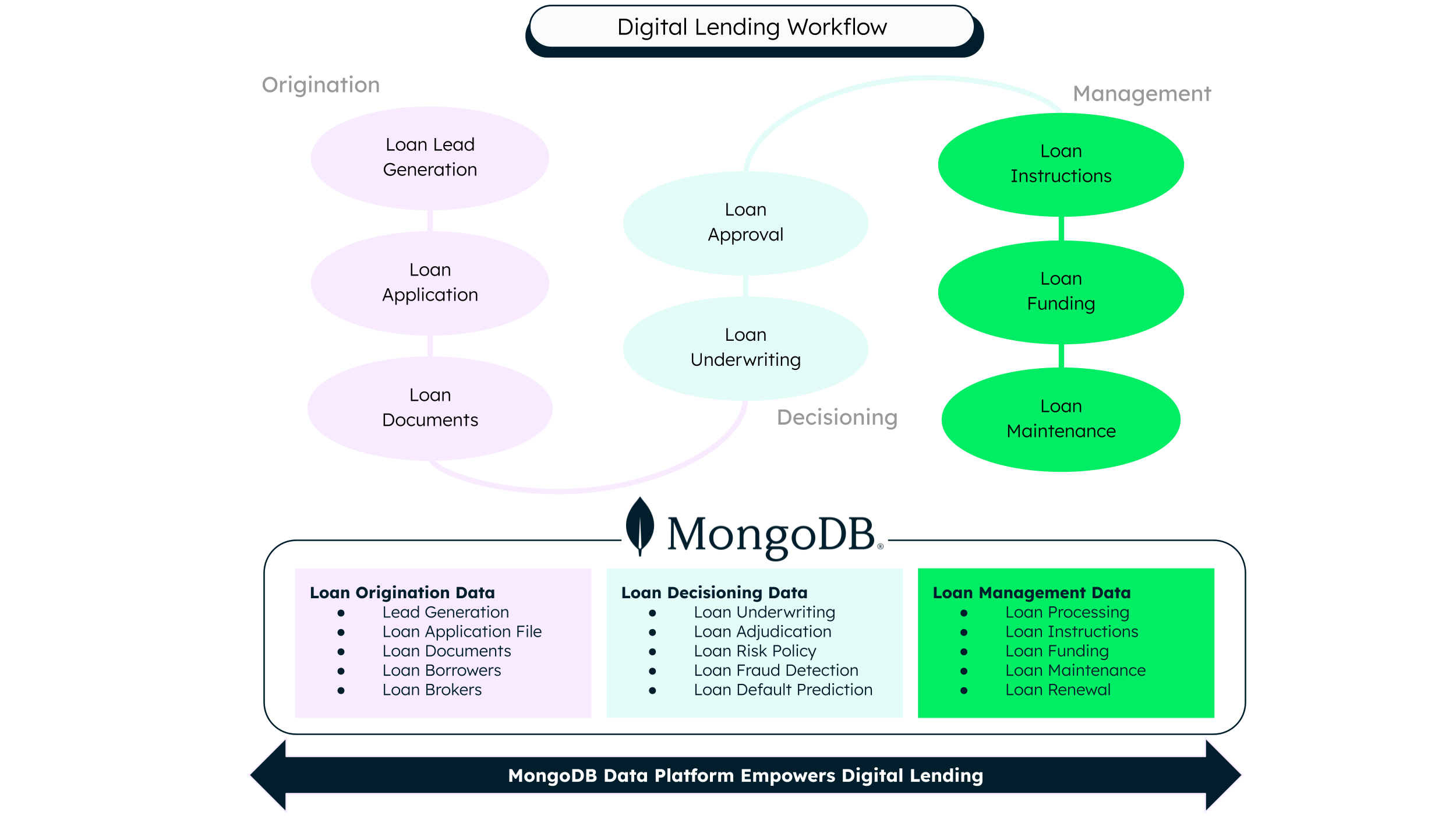

The digital lending lifecycle: from lead to loan management

Modern digital lending has morphed from a linear, paper-heavy process into a data-driven, real-time workflow that spans tightly connected stages. Each stage is powered by automation, data platforms, AI models, and integrated services that remove friction for both borrowers and lenders.

Figure 1. Digital lending workflow powered by MongoDB data platform.

1. Origination: Turning demand into structured data

Origination begins the lending journey. This stage signals when a customer expresses intent and their data first enters the platform. Through digital lead generation across channels, API-driven data capture, and intelligent document processing using AI and e-signatures, lenders can rapidly assemble a complete borrower profile. What’s changing is the move from manual data entry to automated, API-driven ingestion, where documents become machine-readable assets instead of static PDFs, and customer data is captured once and reused across the entire lending lifecycle.

2. Decisioning: From data to risk intelligence

This stage determines whether, how, and at what price a loan should be offered by transforming borrower data into real-time risk intelligence. Through automated or semi-automated digital underwriting combining credit scoring, fraud detection, affordability analysis, and policy rules with AI models for risk segmentation and dynamic pricing, lenders can make fast, consistent decisions. Now batch scoring moves into live decisioning, where traditional credit data is enriched with open banking, behavioral, and alternative data, and AI models continuously learn from repayment behavior and defaults to improve accuracy over time.

3. Approval: Turning risk into a commitment

Once a decision is made, the platform easily moves into contractual execution, transforming risk insights into a formal loan commitment. Automated or assisted approvals generate dynamic loan terms, repayment schedules, and regulatory disclosures, ensuring accuracy and compliance. Things now shift to straight-through processing, manual bottlenecks with loan terms continuously adjusting based on real-time risk signals and regulatory checks embedded directly into the workflow.

4. Funding: Moving money at digital speed

This is the moment when value is realized for the borrower, as funds get disbursed and the loan activates. Modern platforms support multiple funding rails while simultaneously updating core ledgers with real-time balance creation, accounting, and reconciliation. What’s changing is a shift from slow, batch-based settlement to instant, event-driven funding where the loan is no longer a static contract, but a live financial object that updates continuously across systems.

5. Management: The long tail of the loan

After funding, the loan enters its longest phase: servicing and lifecycle management. In the management stage, modern digital lending platforms deliver intelligent loan maintenance and customer engagement through automated payment processing, collections, and refinancing workflows. This all gets supported by self-service portals, real-time notifications, and AI-driven assistance that can also lead to a renewal process. Reactive servicing changes into predictive operations. Here, risk models continuously adapt based on borrower behavior and portfolio managers gain immediate visibility into performance, thus enabling proactive intervention, personalized experiences, and optimized portfolio outcomes.

At the core of all these stages is a unified data layer that easily handles structured and unstructured data from applications and documents to transactions and behavioral events while supporting ever-changing decisions and event-driven workflows. This intelligent data foundation continuously feeds AI systems, compliance engines, and risk analytics, enabling lenders to break away from slow, siloed processes and operate an automated adaptive lending workflow.

Why MongoDB for modern digital lending

In order to move into this new method of digital lending, you need a solid backbone to support the work. MongoDB can help by providing:

A unified data foundation across the lending lifecycle

Digital lending spans applications, documents, transactions, decisions, and servicing events that all have different data structures and change rates. MongoDB’s flexible document model and native support for structured, semi-structured, and unstructured data allow lenders to store and evolve all loan-related data in a single platform. This eliminates data silos, simplifies integrations across origination, underwriting, and servicing systems—and enables a true end-to-end view of every loan.Real-time intelligence for decisioning and agentic AI

Modern lending requires instant decisions and continuous risk assessment. MongoDB’s native change streams, vector search, and hybrid search enable real-time event-driven workflows and AI-powered reasoning across the loan lifecycle. Agentic AI systems can react to new data as it arrives, triggering underwriting updates, fraud checks, pricing changes, or collections actions—without batch delays or complex data pipelines.Scalability, resilience, and regulatory confidence

Lending platforms must scale with demand, remain always available, and meet strict regulatory requirements. MongoDB’s horizontal scalability, global replication, and built-in security features support high-volume lending workloads while maintaining data integrity, auditability, and compliance. This allows lenders to modernize with confidence, knowing their core data platform can grow, adapt, and remain resilient as their business evolves.

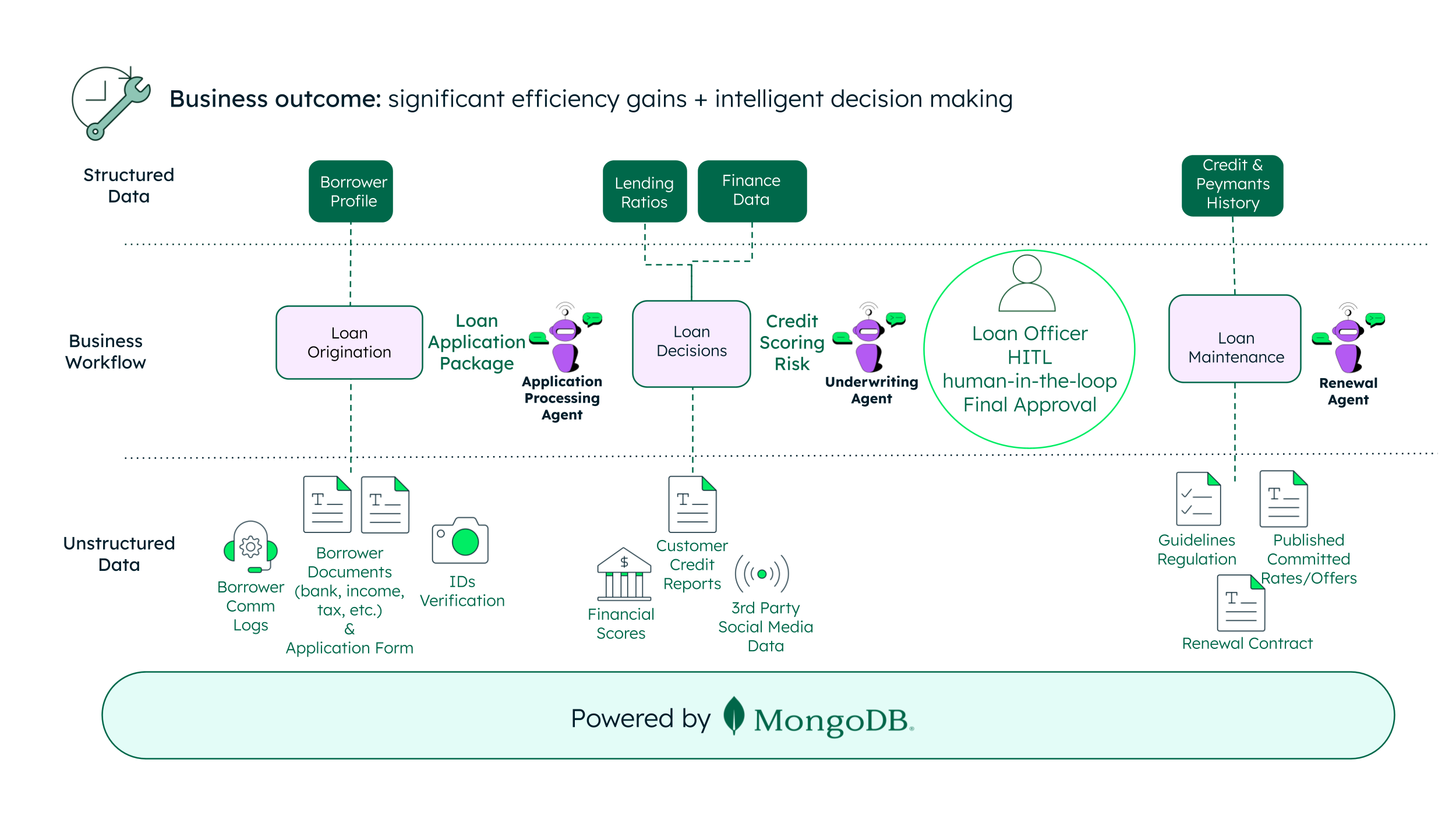

Introducing agentic AI in lending

Agentic AI represents the next evolution of digital lending intelligent systems. These AI agents can reason, act, and adapt across the loan lifecycle, orchestrating tasks from application to underwriting to renewal. By continuously learning from new data and behavioural signals, agentic AI enables lenders to automate complex decisions, proactively manage risk, and deliver highly personalized borrower experiences at scale. Here we introduce three AI agents to support this new digital lending journey.

Figure 2. Agentic AI Workflow - Digital Lending

Loan application agent

The loan application agent acts as the intelligent front door to the lending platform. It guides borrowers through the application process, validates and enriches data in real time, extracts insights from documents using AI, and orchestrates identity validation and eligibility checks. It continuously adapts the application journey based on user behavior and risk signals, reducing friction while ensuring data completeness and regulatory compliance. This agent transforms raw borrower inputs into a trusted, decision-ready loan profile that’s ready to be reviewed by the underwriting agent.

Underwriting agent

The underwriting agent is the always-on risk brain of the lending platform, combining business rules, machine learning models, alternative data, and market signals to dynamically assess creditworthiness, pricing, and risk exposure. As new information becomes available, the underwriting agent continuously recalculates risk and recommends approvals, conditions, and repricing. Or it can decline while routing exceptions and high-risk cases to a human-in-the-loop (HITL) reviewer for final validation and sign off. This hybrid model preserves regulatory control and explainability while still enabling straight-through processing and consistent decisions at scale.

Renewal agent

The renewal agent manages the post-funding lifecycle and proactively optimizes loan performance. It monitors repayment behavior, account activity, and external signals to predict refinancing, upsell, hardship, or churn risk. Based on these insights, the renewal agent can trigger personalized offers, credit limit adjustments, or early intervention strategies turning loan servicing into a predictive, customer-centric growth engine rather than a reactive cost center.

The future of digital lending

Digital lending is rapidly evolving from manual workflows to autonomous, intelligence-driven ecosystems powered by agentic AI. In this next phase, lending platforms will not just respond to customer requests or risk events, they will anticipate them. AI agents will continuously optimize credit policies, personalize borrower journeys, rebalance portfolios, and adapt to economic signals. As data becomes a critical part of every decision and interaction, the lenders that build AI-powered adaptive platforms capable of learning and acting will lead the charge and ultimately succeed. The future of lending is not just digital, it is self-optimizing, proactive, and agentic by design.

Next Steps

1The paradigm shift: How agentic AI is redefining banking operations